Eliminate Risk of Failure with CIMAPRO19-P01-1 Exam Dumps

Schedule your time wisely to provide yourself sufficient time each day to prepare for the CIMAPRO19-P01-1 exam. Make time each day to study in a quiet place, as you'll need to thoroughly cover the material for the P1 Management Accounting exam. Our actual CIMA Professional Qualification exam dumps help you in your preparation. Prepare for the CIMAPRO19-P01-1 exam with our CIMAPRO19-P01-1 dumps every day if you want to succeed on your first try.

All Study Materials

Instant Downloads

24/7 costomer support

Satisfaction Guaranteed

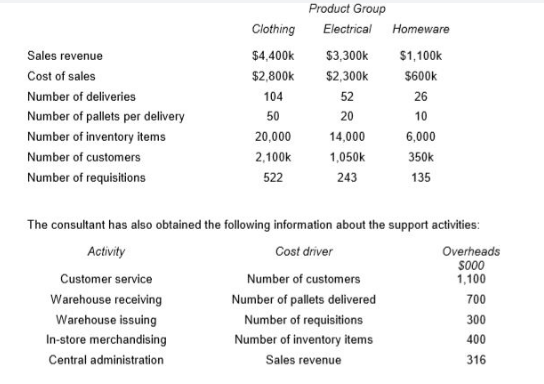

A major company sells a range of electrical, clothing and homeware products through a chain of department stores. The main administration functions are provided from the company's head office. Each department store has its own warehouse which receives goods that are delivered from a central distribution center.

The company currently measures profitability by product group for each store using an absorption costing system. All overhead costs are charged to product groups based on sales revenue. Overhead costs account for approximately one-third of total costs and the directors are concerned about the arbitrary nature of the current method used to charge these costs to product groups.

A consultant has been appointed to analyses the activities that are undertaken in the department stores and to establish an activity based costing system.

The consultant has identified the following data for the latest period for each of the product groups for the X Town store:

Calculate the total profit for each of the product groups:

.... using the current absorption costing system;

CDF is a manufacturing company within the DF group. CDF has been asked to provide a quotation for a contract for a new customer and is aware that this could lead to further orders. As a consequence, CDF will produce the quotation by using relevant costing instead of its usual method of full cost plus pricing. The following information has been obtained in relation to the contract: Material D 40 tons of material D would be required. This material is in regular use by CDF and has a current purchase price of $38 per ton. Currently, there are 5 tons in inventory which cost $35 per ton. The resale value of the material in inventory is $24 per ton.

Components 4,000 components would be required. These could be bought externally for $15 each or alternatively they could be supplied by RDF, another company within the DF manufacturing group. The variable cost of the component if it were manufactured by RDF would be $8 per unit, and RDF adds 30% to its variable cost to contribute to its fixed costs plus a further 20% to this total cost in order to set its internal transfer price. RDF has sufficient capacity to produce 2,500 components without affecting its ability to satisfy its own external customers. However, in order to make the extra 1,500 components required by CDF, RDF would have to forgo other external sales of $50,000 which have a contribution to sales ratio of 40%.

Labour hours 850 direct labour hours would be required. All direct labour within CDF is paid on an hourly basis with no guaranteed wage agreement. The grade of labour required is currently paid $10 per hour, but department W is already working at 100% capacity. Possible ways of overcoming this problem are: * Use workers in department Z, because it has sufficient capacity. These workers are paid $15 per hour. * Arrange for sub-contract workers to undertake some of the other work that is performed in department W. The sub-contract workers would cost $13 per hour.

Specialist machine The contract would require a specialist machine. The machine could be hired for $15,000 or it could be bought for $50,000. At the end of the contract if the machine were bought, it could be sold for $30,000. Alternatively, it could be modified at a cost of $5,000 and then used on other contracts instead of buying another essential machine that would cost $45,000. The operating costs of the machine are payable by CDF whether it hires or buys the machine. These costs would total $12,000 in respect of the new contract.

Supervisor The contract would be supervised by an existing manager who is paid an annual salary of $50,000 and has sufficient capacity to carry out this supervision. The manager would receive a bonus of $500 for the additional work.

Development time 15 hours of development time at a cost of $3,000 have already been worked in determining the resource requirements of the contract.

Fixed overhead absorption rate CDF uses an absorption rate of $20 per direct labour hour to recover its general fixed overhead costs. This includes $5 per hour for depreciation.

Calculate the relevant cost of the contract to CDF. You must present your answer in a schedule that clearly shows the relevant cost value for each of the items identified above. You should also explain each relevant cost value you have included in your schedule and why any values you have excluded are not relevant.

Ignore taxation and the time value of money.

Select all the true statements.

See the explanation below.

References:

Explain how probability analysis could be used to assess the risk of the evaluated projects.

Select all the true statements.

See the explanation below.

References:

Select the benefits to a company of using sensitivity analysis in investment appraisal.

(Select all the true statements.)

See the explanation below.

References:

Calculate the sensitivity of the investment decision to a change in the annual fixed costs.

By how much should the present value of the fixed cost increase, before this project is not viable?

See the explanation below.

References:

Are You Looking for More Updated and Actual CIMAPRO19-P01-1 Exam Questions?

If you want a more premium set of actual CIMAPRO19-P01-1 Exam Questions then you can get them at the most affordable price. Premium CIMA Professional Qualification exam questions are based on the official syllabus of the CIMAPRO19-P01-1 exam. They also have a high probability of coming up in the actual P1 Management Accounting exam.

You will also get free updates for 90 days with our premium CIMAPRO19-P01-1 exam. If there is a change in the syllabus of CIMAPRO19-P01-1 exam our subject matter experts always update it accordingly.