- Home /

- CFA Institute /

- Chartered Financial Analyst Level II /

- CFA-Level-II Dumps

Eliminate Risk of Failure with CFA Institute CFA-Level-II Exam Dumps

Schedule your time wisely to provide yourself sufficient time each day to prepare for the CFA Institute CFA-Level-II exam. Make time each day to study in a quiet place, as you'll need to thoroughly cover the material for the CFA Level II Chartered Financial Analyst exam. Our actual CFA Level II exam dumps help you in your preparation. Prepare for the CFA Institute CFA-Level-II exam with our CFA-Level-II dumps every day if you want to succeed on your first try.

All Study Materials

Instant Downloads

24/7 costomer support

Satisfaction Guaranteed

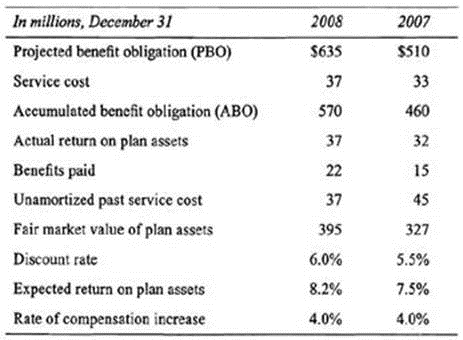

Lauren Jacobs, CFA, is an equity analyst for DF Investments. She is evaluating Iron Parts Inc. Iron Parts is a manufacturer of interior systems and components for automobiles. The company is the world's second largest original equipment auto parts supplier, with a market capitalization of $1.8 billion. Based on Iron Parts's low price-to-book value ratio of 0.9* and low price-to-sales ratio of 0.15x, Jacobs believes the stock could be an interesting investment. However, she wants to review the disclosures found in the company's financial footnotes. In particular, Jacobs is concerned about Iron Parts's defined benefit pension plan. The following information for 2007 and 2008 is provided.

Iron Parts has adopted SFAS No. 158, Employers' Accounting for Defined Benefit Pensions and Other Postretirement Plans.

Jacobs wants to fully understand the impact of changing pension assumptions on Iron Parts's balance sheet and income statement. In addition, she would like to compute Iron Parts's economic pension expense.

As of December 31, 2008, the funded status of Iron Parts's pension plan was:

See the explanation below.

Funded status equals fair value of plan assets minus PBO (395 - 635 = -240). (Study Session 6, LOS 22.c,f)

Paul Durham, CFA, is a senior manager in the structured bond department within Newton Capital Partners (NCP), an investment banking firm located in the United States. Durham has just returned from an international marketing campaign for NCP's latest structured note offering, a series of equity linked fixed-income securities or ELFS. The bonds will offer a 4.5% coupon paid annually along with the annual return on the S&P 500 Index and will have a maturity of five years. The total face value of the ELFS series is expected to be $200 million.

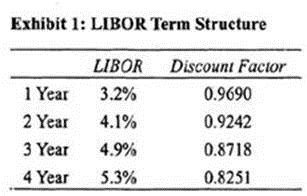

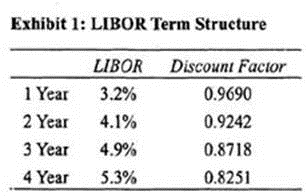

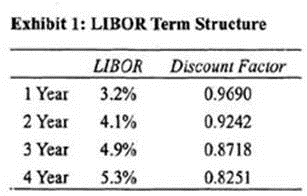

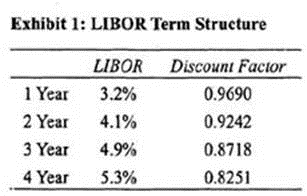

Susan Jacobs, a fixed-income portfolio manager and principal with Smith & Associates, has decided to include $10 million worth of ELFS in her fixed-income portfolio. At the end of the first year, however, the S&P 500 Index value is 1,054, significantly lower than the initial value of 1,112 set by NCP at the time of the ELFS offering. Jacobs is concerned that the four remaining years of the ELFS life could have similar results and is considering her alternatives to offset the equity exposure of the ELFS position without selling the bonds, Jacobs decides to offset her portfolio's exposure to the ELFS by entering into an equity swap contract. The LIBOR term structure is shown below in Exhibit 1.

After hearing of her plan, one of the other partners with Smith & Associates, Jonathan Widby, feels it is necessary to meet with Jacobs regarding her proposed strategy. Mr. Widby makes the following comments during the meeting:

"You should also know that I am quite bullish on the stock market for the near future. Therefore, as an alternative strategy, I recommend that you establish a long position in a 1 x 3 payer swaption. This strategy would allow you to wait and see how the market performs next year but will give you the ability to enter into a 2-year swap with terms that can be established today should the market have another down year.

If, however, you choose to proceed with your strategy, know that credit risk for an equity swap is greatest toward the end of the swap's life. Thus, analysts tracking your portfolio will not be happy with the added credit risk (hat your portfolio will be exposed to as the swap nears the end of its tenor. You should think about what credit derivatives you can use to manage this risk when the time comes."

To offset any credit risk associated with the equity swap, Widby recommends using an index trade strategy by entering into a credit default swap (CDS) as a protection buyer. Widby's strategy would involve purchasing credit protection on an index comprising largely the same issuers (companies) included in the equity index underlying the swap. Widby suggests the CDS should have a maturity equal to that of the swap to provide maximum credit protection.

Evaluate, in light of the appropriate equity swap strategy for Jacobs's portfolio, Mr. Widby's comments regarding the credit risk and use of swaptions in Jacobs's portfolio.

See the explanation below.

Credit risk in a swap is generally highest in rhe middle of the swap. At the end of the swap there are few potential payments left and the probability of either party defaulting on their commitment is relatively low. Therefore, Widby's first comment is incorrect. It Jacobs wants to delay establishing a swap position, a swaption would potentially be an appropriate investment. However, Jacobs should buy a receiver swaption, not a payer swaption. In a payer swaption, Jacobs would pay the fixed-rate and receive the equity index return. The swap underlying a payer swaption would not offset Jacobs's current position. (Study Session 17, LOS 6l.f,i)

Paul Durham, CFA, is a senior manager in the structured bond department within Newton Capital Partners (NCP), an investment banking firm located in the United States. Durham has just returned from an international marketing campaign for NCP's latest structured note offering, a series of equity linked fixed-income securities or ELFS. The bonds will offer a 4.5% coupon paid annually along with the annual return on the S&P 500 Index and will have a maturity of five years. The total face value of the ELFS series is expected to be $200 million.

Susan Jacobs, a fixed-income portfolio manager and principal with Smith & Associates, has decided to include $10 million worth of ELFS in her fixed-income portfolio. At the end of the first year, however, the S&P 500 Index value is 1,054, significantly lower than the initial value of 1,112 set by NCP at the time of the ELFS offering. Jacobs is concerned that the four remaining years of the ELFS life could have similar results and is considering her alternatives to offset the equity exposure of the ELFS position without selling the bonds, Jacobs decides to offset her portfolio's exposure to the ELFS by entering into an equity swap contract. The LIBOR term structure is shown below in Exhibit 1.

After hearing of her plan, one of the other partners with Smith & Associates, Jonathan Widby, feels it is necessary to meet with Jacobs regarding her proposed strategy. Mr. Widby makes the following comments during the meeting:

"You should also know that I am quite bullish on the stock market for the near future. Therefore, as an alternative strategy, I recommend that you establish a long position in a 1 x 3 payer swaption. This strategy would allow you to wait and see how the market performs next year but will give you the ability to enter into a 2-year swap with terms that can be established today should the market have another down year.

If, however, you choose to proceed with your strategy, know that credit risk for an equity swap is greatest toward the end of the swap's life. Thus, analysts tracking your portfolio will not be happy with the added credit risk (hat your portfolio will be exposed to as the swap nears the end of its tenor. You should think about what credit derivatives you can use to manage this risk when the time comes."

To offset any credit risk associated with the equity swap, Widby recommends using an index trade strategy by entering into a credit default swap (CDS) as a protection buyer. Widby's strategy would involve purchasing credit protection on an index comprising largely the same issuers (companies) included in the equity index underlying the swap. Widby suggests the CDS should have a maturity equal to that of the swap to provide maximum credit protection.

Jacobs has observed declining swap spreads on several of the equity swaps that she is considering as potential investments. What do the declining swap spreads indicate?

See the explanation below.

The swap spread represents the general level of credit risk in the marketplace. The fixed rate on any particular swap is the same for any interested party regardless of their credit quality. Therefore, the swap spread (the difference between the fixed rate and the reference rate) is a general measure of credit quality in the global economy. (Study Session 17, LOS 61.j)

Paul Durham, CFA, is a senior manager in the structured bond department within Newton Capital Partners (NCP), an investment banking firm located in the United States. Durham has just returned from an international marketing campaign for NCP's latest structured note offering, a series of equity linked fixed-income securities or ELFS. The bonds will offer a 4.5% coupon paid annually along with the annual return on the S&P 500 Index and will have a maturity of five years. The total face value of the ELFS series is expected to be $200 million.

Susan Jacobs, a fixed-income portfolio manager and principal with Smith & Associates, has decided to include $10 million worth of ELFS in her fixed-income portfolio. At the end of the first year, however, the S&P 500 Index value is 1,054, significantly lower than the initial value of 1,112 set by NCP at the time of the ELFS offering. Jacobs is concerned that the four remaining years of the ELFS life could have similar results and is considering her alternatives to offset the equity exposure of the ELFS position without selling the bonds, Jacobs decides to offset her portfolio's exposure to the ELFS by entering into an equity swap contract. The LIBOR term structure is shown below in Exhibit 1.

After hearing of her plan, one of the other partners with Smith & Associates, Jonathan Widby, feels it is necessary to meet with Jacobs regarding her proposed strategy. Mr. Widby makes the following comments during the meeting:

"You should also know that I am quite bullish on the stock market for the near future. Therefore, as an alternative strategy, I recommend that you establish a long position in a 1 x 3 payer swaption. This strategy would allow you to wait and see how the market performs next year but will give you the ability to enter into a 2-year swap with terms that can be established today should the market have another down year.

If, however, you choose to proceed with your strategy, know that credit risk for an equity swap is greatest toward the end of the swap's life. Thus, analysts tracking your portfolio will not be happy with the added credit risk (hat your portfolio will be exposed to as the swap nears the end of its tenor. You should think about what credit derivatives you can use to manage this risk when the time comes."

To offset any credit risk associated with the equity swap, Widby recommends using an index trade strategy by entering into a credit default swap (CDS) as a protection buyer. Widby's strategy would involve purchasing credit protection on an index comprising largely the same issuers (companies) included in the equity index underlying the swap. Widby suggests the CDS should have a maturity equal to that of the swap to provide maximum credit protection.

If Jacobs enters into a $10 million 4-year annual-pay floating-rate equity swap based on 1-year LIBOR and the total return on the S&P 500 Index, what is the value of the remaining 3-year swap to the floating rate payer after one year if the Index has increased from 1,054 to 1,103 and the LIBOR term structure is as given below?

LIBOR

1-year: 4.1%

2-ycar: 4.7%

3-year: 5.3%

See the explanation below.

A floating-rare equity swap will have zero value on the reset date. The value of the floating-rate side is par or $10 million. The value of a $10 million exposure to the Index is also $10 million. Intuitively, this position could be established by borrowing for three years ar a floaring rate of 1-year LIBOR and investing the proceeds in the index, a zero value portfolio. (Study Session 17, LOS 61.e)

Paul Durham, CFA, is a senior manager in the structured bond department within Newton Capital Partners (NCP), an investment banking firm located in the United States. Durham has just returned from an international marketing campaign for NCP's latest structured note offering, a series of equity linked fixed-income securities or ELFS. The bonds will offer a 4.5% coupon paid annually along with the annual return on the S&P 500 Index and will have a maturity of five years. The total face value of the ELFS series is expected to be $200 million.

Susan Jacobs, a fixed-income portfolio manager and principal with Smith & Associates, has decided to include $10 million worth of ELFS in her fixed-income portfolio. At the end of the first year, however, the S&P 500 Index value is 1,054, significantly lower than the initial value of 1,112 set by NCP at the time of the ELFS offering. Jacobs is concerned that the four remaining years of the ELFS life could have similar results and is considering her alternatives to offset the equity exposure of the ELFS position without selling the bonds, Jacobs decides to offset her portfolio's exposure to the ELFS by entering into an equity swap contract. The LIBOR term structure is shown below in Exhibit 1.

After hearing of her plan, one of the other partners with Smith & Associates, Jonathan Widby, feels it is necessary to meet with Jacobs regarding her proposed strategy. Mr. Widby makes the following comments during the meeting:

"You should also know that I am quite bullish on the stock market for the near future. Therefore, as an alternative strategy, I recommend that you establish a long position in a 1 x 3 payer swaption. This strategy would allow you to wait and see how the market performs next year but will give you the ability to enter into a 2-year swap with terms that can be established today should the market have another down year.

If, however, you choose to proceed with your strategy, know that credit risk for an equity swap is greatest toward the end of the swap's life. Thus, analysts tracking your portfolio will not be happy with the added credit risk (hat your portfolio will be exposed to as the swap nears the end of its tenor. You should think about what credit derivatives you can use to manage this risk when the time comes."

To offset any credit risk associated with the equity swap, Widby recommends using an index trade strategy by entering into a credit default swap (CDS) as a protection buyer. Widby's strategy would involve purchasing credit protection on an index comprising largely the same issuers (companies) included in the equity index underlying the swap. Widby suggests the CDS should have a maturity equal to that of the swap to provide maximum credit protection.

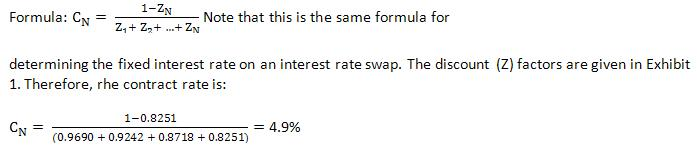

Based on the strategy appropriate for Jacobs's portfolio, determine the contract rate on the swap strategy.

See the explanation below.

Calculate the contract rate on a fixed-rate receiver equity swap using the following

(Study Session 17, LOS 6l.c)

Are You Looking for More Updated and Actual CFA Institute CFA-Level-II Exam Questions?

If you want a more premium set of actual CFA Institute CFA-Level-II Exam Questions then you can get them at the most affordable price. Premium CFA Level II exam questions are based on the official syllabus of the CFA Institute CFA-Level-II exam. They also have a high probability of coming up in the actual CFA Level II Chartered Financial Analyst exam.

You will also get free updates for 90 days with our premium CFA Institute CFA-Level-II exam. If there is a change in the syllabus of CFA Institute CFA-Level-II exam our subject matter experts always update it accordingly.